Are you wondering how much life insurance might cost you each month? Knowing the average price can help you plan better and protect your loved ones without breaking the bank.

But the truth is, life insurance costs aren’t one-size-fits-all—they depend on several factors that affect your personal rate. Keep reading to discover what influences your monthly premium and how you can find a plan that fits your budget and gives you peace of mind.

Your family’s future is worth understanding these details.

Factors Influencing Life Insurance Costs

Understanding what affects your life insurance cost can help you make smarter choices. Several factors come into play, shaping your monthly premium. Knowing these can save you money and ensure you get the right coverage.

Age And Its Impact

Age is one of the biggest factors in life insurance pricing. The younger you are, the cheaper your premiums tend to be because you are seen as lower risk. If you wait until your 40s or 50s, expect to pay more each month.

I once helped a friend buy life insurance in his early 30s, and his monthly cost was half what it was when his older brother bought a similar policy in his late 40s. This shows how acting sooner can lower your expenses.

Health And Medical History

Your health status directly influences your insurance costs. If you have a history of chronic illnesses or recent medical issues, insurers may charge higher premiums or even deny coverage. On the other hand, good health and regular check-ups can keep costs down.

Think about your last doctor’s visit. Did you mention any ongoing conditions? These details matter a lot to insurance companies when calculating your risk.

Coverage Amount

The amount of coverage you choose impacts your monthly payment. Higher coverage means the insurer takes on more risk, so your premiums go up. Choosing the right amount is a balance between protecting your loved ones and staying within your budget.

- Smaller coverage suits short-term needs or tight budgets.

- Larger coverage fits long-term financial security plans.

Ask yourself: How much money would your family need if you weren’t there? That figure guides your coverage choice.

Policy Type Differences

Term life and whole life insurance work differently and cost differently. Term life is usually cheaper because it covers you for a set period. Whole life costs more since it lasts your entire life and builds cash value.

If you want a straightforward, affordable option, term life might be better. But if you want lifelong coverage with an investment element, whole life could be worth the higher price.

Lifestyle And Occupation

Your daily habits and job affect your risk profile. Smokers, heavy drinkers, or people with risky hobbies pay more. Similarly, dangerous jobs like construction or firefighting raise premiums due to higher accident chances.

Think about your routine. Do you smoke or have a high-risk hobby? Being honest with your insurer can avoid surprises later and help you find ways to reduce your costs.

Average Monthly Premiums By Age Group

Life insurance costs vary by age. Younger people pay less because they are healthier. Older people pay more due to higher health risks. Understanding average monthly premiums by age helps plan your budget better.

Insurance companies use age to calculate risk. Age affects how much you pay every month. Below are typical costs for different age groups.

20s And 30s

People in their 20s and 30s get the lowest rates. Monthly premiums can range from $15 to $30. Health is usually good, so companies charge less. Buying early locks in low prices for the future.

40s And 50s

Costs rise in your 40s and 50s. Monthly premiums often range from $30 to $75. Health problems may start appearing. Insurance companies see more risk with age. The older you get, the higher the monthly cost.

60 And Above

Premiums jump significantly after 60. Expect to pay $75 to $200 or more per month. Health issues are common at this age. Some insurers may limit coverage or increase prices. It is still possible to find affordable options with good research.

Cost Comparison Of Term Vs. Whole Life Insurance

Choosing between term and whole life insurance often depends on cost. Both types serve different purposes but differ greatly in price. Understanding their monthly premiums helps decide which fits your budget and needs.

Term Life Premium Trends

Term life insurance offers coverage for a set period, like 10 or 20 years. Its monthly premiums tend to be lower than whole life. Younger, healthier people usually pay less. Premiums stay level for the term length but rise sharply after. This makes term life affordable for many families.

Whole Life Premium Trends

Whole life insurance covers you for your entire life. It combines a death benefit with a savings component. Monthly premiums are higher than term life. These premiums stay the same throughout your life. The savings part grows slowly but adds to the policy’s value. Whole life suits those wanting lifelong coverage and forced savings.

Which Is More Cost-effective?

Term life insurance is usually cheaper month to month. It works well for short-term needs, like raising children. Whole life costs more but builds cash value over time. It fits those planning long-term and wanting investment benefits. For tight budgets, term life offers strong protection at a low cost.

Ways To Lower Your Life Insurance Premium

Lowering your life insurance premium can save money every month. Small changes can make a big difference. This guide shares simple ways to reduce your costs without losing coverage.

Start with your health, choose the right plan, bundle policies, and compare prices. These steps help keep your premium affordable.

Improving Health Metrics

Your health affects your life insurance cost a lot. Quitting smoking lowers risk and cuts premiums. Maintaining a healthy weight also helps. Regular exercise and good diet improve your health numbers. Better health means lower monthly payments.

Choosing Appropriate Coverage

Pick a policy that fits your needs. Avoid too much coverage that increases your premium. Term life insurance usually costs less than whole life. Match coverage length to your financial goals. Right coverage saves money without risking your family’s security.

Bundling Policies

Combine life insurance with other insurance like auto or home. Many companies offer discounts for bundled policies. Bundling reduces your total insurance cost each month. It also simplifies payments and paperwork.

Shopping Around

Prices vary by company. Compare quotes from several insurers before buying. Use online tools for fast price checks. Different companies see risk in different ways. Shopping saves money and finds the best deal for you.

Additional Fees And Riders Affecting Monthly Costs

Life insurance costs are not just about the base premium. Extra fees and riders can change the monthly price. These additions customize your policy. They provide extra protection or benefits. But they also add to your monthly cost. Knowing what affects your premium helps you plan better.

Common Riders And Their Costs

Riders add special features to your life insurance. They protect against specific risks. One popular rider is the accidental death benefit. It pays more if death is due to an accident. This can increase monthly costs by $5 to $15.

The waiver of premium rider stops payments if you become disabled. This rider costs around $10 to $20 per month. Another rider is the child term rider. It covers your children for a small extra fee, often $2 to $5 monthly.

Some riders, like chronic illness riders, allow early payout. These can raise costs by $15 to $30 monthly. Each rider adds value but also raises your monthly bill. Choose riders based on your needs and budget.

Understanding Policy Fees

Life insurance policies often have fees beyond premiums. These fees cover administration and company costs. One common fee is the policy fee. It can be $5 to $10 per month. This fee stays the same regardless of your coverage size.

Some policies have surrender charges. These fees apply if you cancel early. They reduce the amount you get back. Other fees include underwriting and medical exam costs. These are usually one-time but can affect your initial cost.

Knowing these fees helps avoid surprises. Ask your insurer to explain all possible charges. This knowledge helps you pick the best plan for your money.

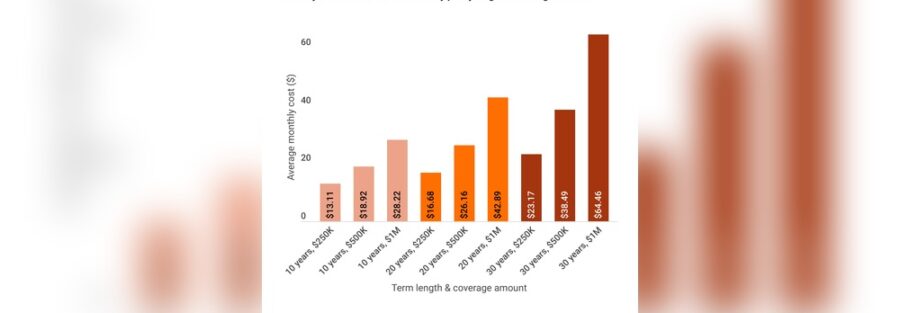

Credit: www.policyadvisor.com

Impact Of Gender And Family History On Premiums

Gender and family history play a big role in life insurance costs. Insurers use these factors to decide how risky it is to insure someone. This risk affects the monthly premiums you pay. Understanding these impacts helps you get better rates and plan your budget.

How Gender Affects Life Insurance Premiums

Women usually pay less for life insurance than men. This is because women tend to live longer. Insurance companies see men as higher risk. Men have more health issues and shorter lifespans on average. This makes their premiums higher than women’s.

Role Of Family Health History

Insurance companies ask about your family’s health history. They check for diseases like cancer, heart problems, or diabetes. If these run in your family, your premium may increase. A family history of serious illness signals a higher risk. This means you might pay more each month.

Why These Factors Matter For Your Budget

Knowing how gender and family history affect premiums helps you plan. You can expect higher or lower costs based on these details. This knowledge allows you to shop around for better deals. It also helps you choose the right coverage amount.

How Insurance Companies Calculate Monthly Rates

Insurance companies use specific methods to set monthly life insurance rates. They study many factors to decide how much risk a person brings. This helps them create fair prices for each policyholder. Understanding these steps can help you see why costs differ.

Risk Assessment Models

Risk assessment models help insurers predict future claims. They use data like age, health, and lifestyle. Younger, healthy people usually have lower risk scores. Smokers or people with serious illnesses get higher scores. These models also consider job type and hobbies. High-risk jobs or dangerous hobbies raise monthly rates.

Underwriting Process

Underwriting is the step where the insurer reviews your application. They check medical records, family history, and habits. Sometimes, a medical exam is required. This process confirms the risk level assigned by models. The underwriter adjusts rates based on this detailed review. This ensures that rates match the real risk you represent.

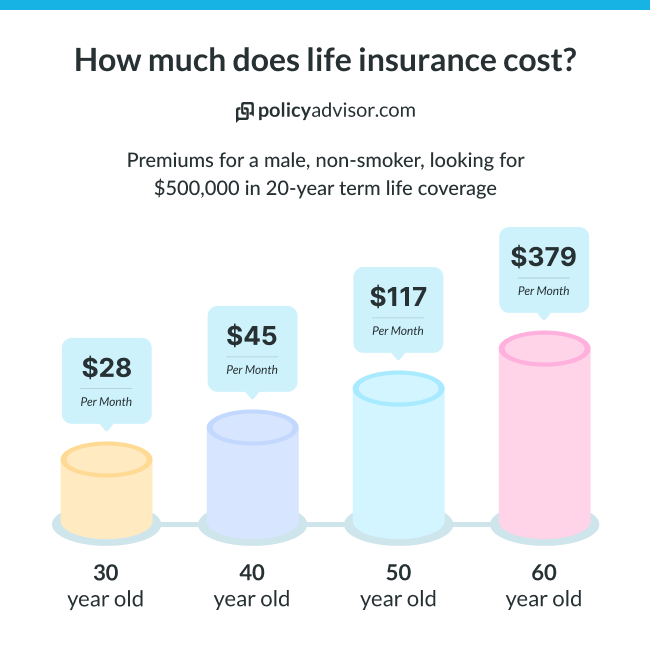

Credit: fidelitylife.com

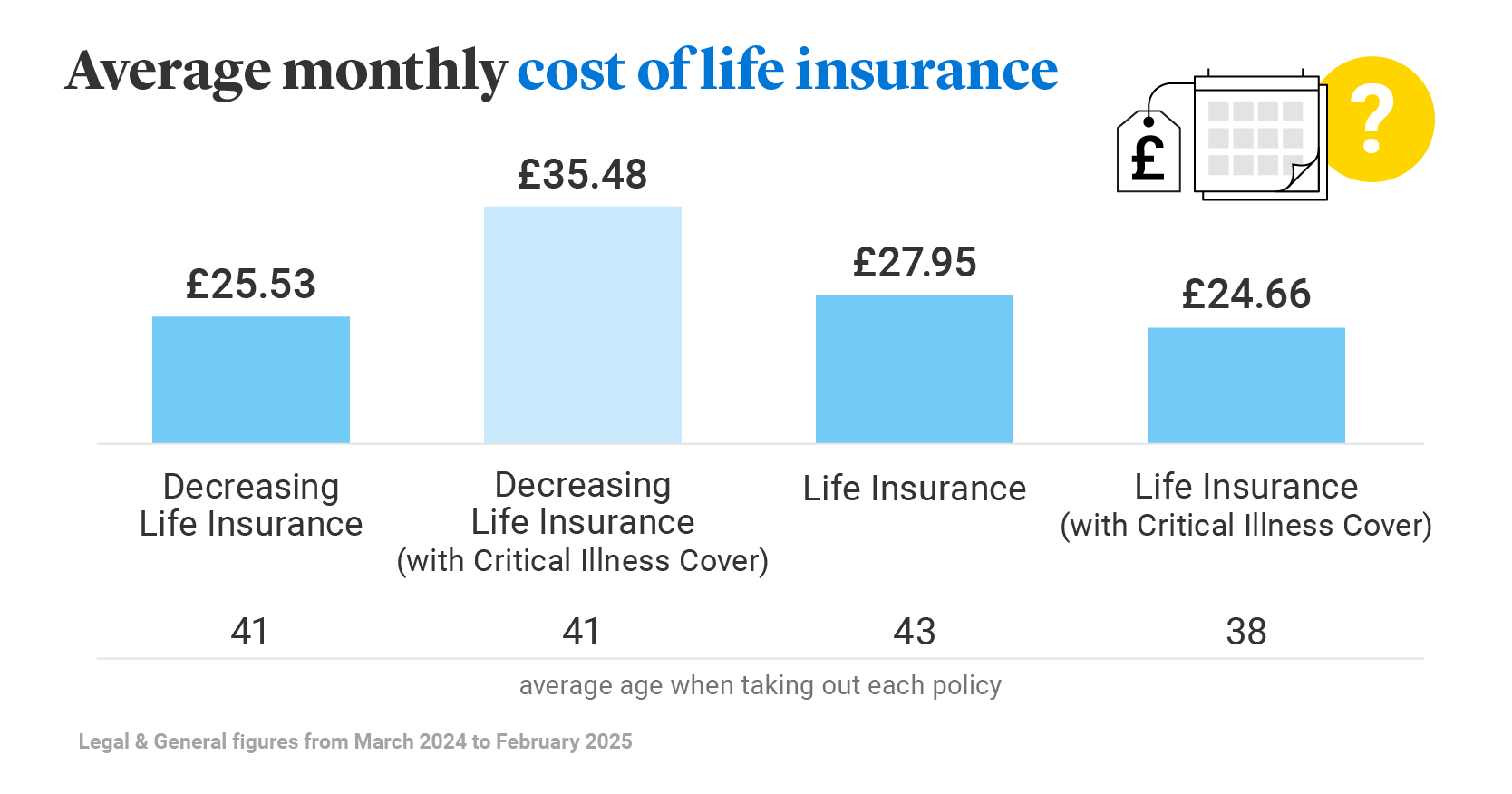

Credit: www.legalandgeneral.com

Frequently Asked Questions

What Factors Influence Life Insurance Monthly Costs?

Life insurance costs depend on age, health, policy type, coverage amount, and lifestyle. Younger, healthier individuals pay less. Term life is cheaper than whole life. Smoking and risky jobs increase premiums. Each factor shapes your monthly payment significantly.

How Much Does Term Life Insurance Cost Monthly?

Term life insurance typically costs between $15 and $50 per month. Rates vary by age, coverage, and health. Younger applicants pay lower premiums. Term policies offer affordable, temporary coverage, making them popular for budget-conscious buyers.

Does Age Affect Monthly Life Insurance Premiums?

Yes, age greatly affects premiums. Younger people pay lower rates because they’re less risky. As you age, premiums rise due to increased health risks. Buying earlier saves money over the policy’s life.

Can Lifestyle Choices Lower Life Insurance Costs?

Yes, healthy habits like not smoking and regular exercise reduce premiums. Insurers reward low-risk lifestyles with lower monthly costs. Avoiding risky activities also helps keep rates affordable.

Conclusion

Life insurance costs vary based on age, health, and coverage amount. Younger and healthier people usually pay less each month. Choosing the right plan helps balance cost and protection. Monthly payments can fit many budgets with careful planning. Knowing average prices helps you prepare better for the future.

Think about what your family needs most. A small monthly cost can bring peace of mind. Take time to compare offers before deciding. Life insurance can protect your loved ones when it matters most.