Indexed Universal Life is so misunderstood! Make sure you are working with someone who knows what they are doing. Not sure if …

Indexed Universal Life (IUL) insurance is a type of permanent life insurance policy that offers flexible premiums, an adjustable death benefit, and the potential for cash value growth based on the performance of a stock market index. While this type of insurance can provide financial protection for your loved ones, it is important to understand the fees associated with an IUL policy.

One of the key benefits of an IUL policy is the ability to accumulate cash value over time. This cash value can be accessed through withdrawals or loans, providing a source of funds for emergencies or other financial needs. However, the growth of the cash value is not guaranteed and is dependent on the performance of the chosen stock market index.

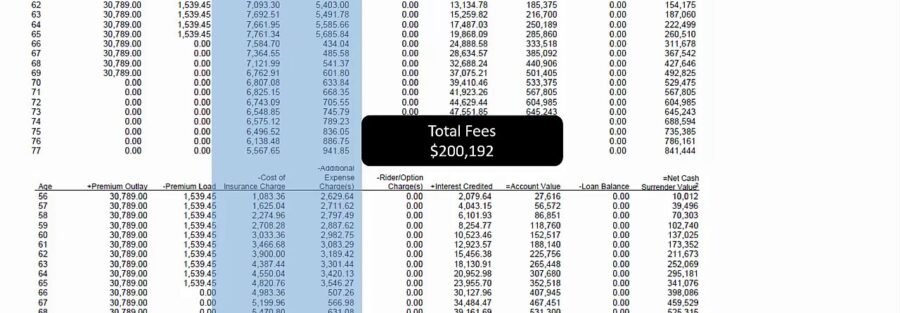

To cover the costs of administering the policy and providing insurance coverage, insurance companies charge various fees that can impact the overall returns of an IUL policy. Here are some common fees associated with IUL insurance:

1. Premium Charge: This fee is deducted from each premium payment made by the policyholder. The premium charge covers the cost of insuring the policyholder and managing the policy.

2. Cost of Insurance (COI): The COI is the cost of providing the death benefit coverage included in the policy. This fee is based on the insured’s age, gender, health, and the amount of coverage.

3. Administrative Fees: These fees cover the administrative costs of managing the policy, such as processing premium payments, issuing statements, and providing customer service.

4. Rider Fees: Riders are additional benefits that can be added to an IUL policy for an extra cost. Common riders include accelerated death benefit riders, long-term care riders, and disability income riders.

5. Indexing Fees: Since the cash value in an IUL policy is tied to the performance of a stock market index, there may be fees associated with tracking the index and crediting the cash value accordingly.

Understanding these fees is essential when considering an IUL policy, as they can significantly impact the policy’s performance. It is important to work with an experienced insurance agent who can explain the fees and help you navigate the complexities of an IUL policy.

When comparing IUL policies from different insurance companies, it is important to consider not only the fees but also the projected cash value growth, death benefit options, and surrender charges. Some policies may have lower fees but offer lower growth potential, while others may have higher fees but offer better performance.

In conclusion, Indexed Universal Life insurance can be a valuable tool for providing financial protection and building cash value over time. However, it is important to understand the fees associated with an IUL policy and how they can impact the overall performance of the policy. By working with a knowledgeable insurance agent and carefully comparing policy options, you can make an informed decision about whether an IUL policy is the right choice for your financial needs.