Life insurance study sessions can be overwhelming, especially when delving into complex topics such as annuities and provisions. However, understanding these concepts is crucial for anyone looking to secure their financial future and protect their loved ones. In this article, we will break down the key points of annuities and provisions in life insurance, helping you navigate this important aspect of financial planning.

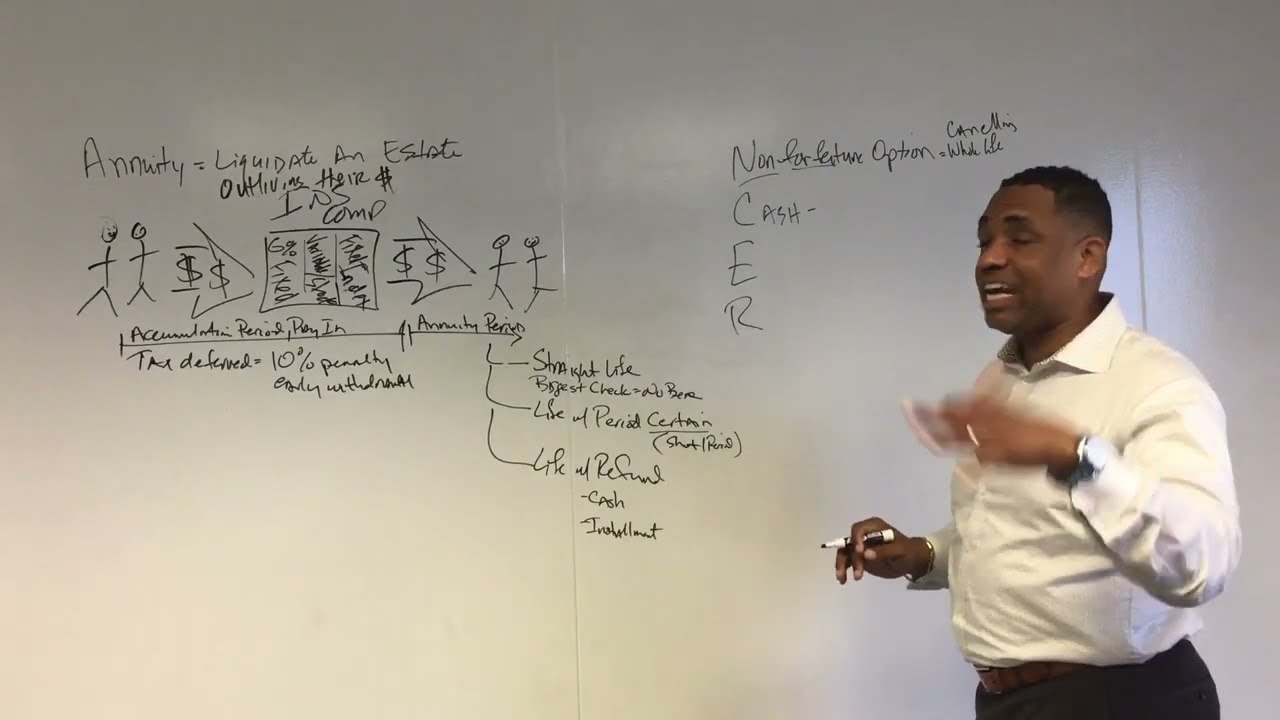

Annuities are a popular financial product that can provide a steady stream of income during retirement. They are essentially a contract between an individual and an insurance company, where the individual makes a lump sum payment or a series of payments in exchange for regular payouts, typically starting at retirement age. There are several types of annuities, including fixed, variable, and indexed annuities, each with its own set of features and benefits.

Fixed annuities offer a guaranteed interest rate and principal protection, making them a low-risk option for individuals looking for a stable income stream. Variable annuities, on the other hand, allow individuals to invest their premiums in various sub-accounts, similar to mutual funds. While variable annuities offer the potential for higher returns, they also come with greater risk. Indexed annuities are a hybrid of fixed and variable annuities, offering a guaranteed minimum return along with the potential for higher returns based on the performance of a specific market index.

When considering an annuity, it is important to carefully review the contract terms, fees, and surrender charges. Annuities can be complex financial products, and it is essential to fully understand how they work before making a decision. Additionally, annuities are not suitable for everyone, and individuals should consider their financial goals and risk tolerance before purchasing an annuity.

Provisions are another important aspect of life insurance policies that can have a significant impact on the policyholder’s coverage and benefits. Provisions are essentially clauses in the policy that outline the rights and obligations of the insurance company and the policyholder. Some common provisions include the grace period, incontestability clause, suicide clause, and premium payment provisions.

The grace period provision allows the policyholder to make a late payment without forfeiting their coverage. Typically, a grace period of 30-31 days is provided, during which the policyholder can pay their premium without penalty. The incontestability clause prevents the insurance company from contesting the validity of the policy after a certain period, typically two years. The suicide clause states that the policy benefits will not be paid if the insured commits suicide within a specified period after the policy is issued.

Understanding these provisions is essential for policyholders to ensure they are fully aware of their rights and obligations under the policy. Additionally, reviewing the provisions can help policyholders make informed decisions about their coverage and benefits. It is also important to review the provisions regularly, as they may change over time or vary between insurance companies.

In conclusion, annuities and provisions are essential components of life insurance policies that can significantly impact an individual’s financial security. By understanding how annuities work and reviewing the key provisions of their policy, individuals can make informed decisions about their coverage and benefits. Life insurance study sessions may be daunting, but with a clear understanding of these concepts, individuals can better navigate the complex world of financial planning and protect their loved ones for years to come.

Frequently Asked Questions

How much life insurance do I need?

Most financial advisors recommend 10-12x your annual income in life insurance coverage. This ensures your family can maintain their lifestyle, pay off debts, and fund future goals like college education. Use our free quote tool to find the right coverage amount for your budget.

What type of life insurance is best?

The best type depends on your needs. Term life is cheapest and best for temporary needs (mortgage, income replacement). Whole life provides lifelong coverage with cash value. Universal life offers flexibility. Compare quotes from multiple providers to find your best option.

How do I get the cheapest life insurance?

To get the cheapest rates: buy while you’re young and healthy, compare quotes from at least 5 providers, choose term life over permanent, maintain a healthy lifestyle, and consider annual premiums instead of monthly. Our comparison tool makes it easy to find the lowest rates.

Compare Free Life Insurance Quotes Today

Get personalized rates from 50+ providers. No obligation, no medical exam required.

🛡️ Get Your Free Life Insurance Quote →

🔒 256-bit SSL Encrypted | ⭐ 4.8/5 Rating | 🏆 50+ Providers