To fully appreciate IUL, you really need to understand the indexed universal life insurance 7 pay premium and how it can be …

Understanding Indexed Universal Life Insurance 7 Pay Premium

Indexed Universal Life Insurance, or IUL, is a type of permanent life insurance policy that offers both a death benefit and a cash value component. One key feature of an IUL policy is the ability to participate in the gains of a stock market index, while being protected from market losses. When considering an IUL policy, it is important to understand the various premium payment options available, including the 7-pay premium option.

What is a 7-pay premium?

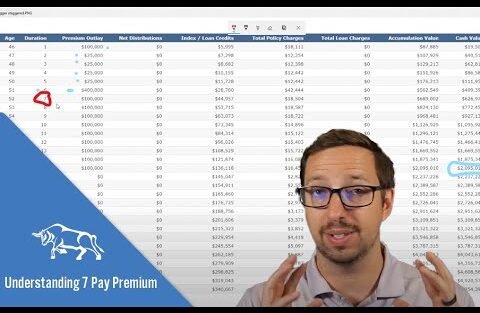

A 7-pay premium refers to a premium payment schedule in which the policyholder pays the required premiums for the first seven years of the policy. Once the seven years are up, the policy is considered fully paid up, meaning the policyholder no longer has to make premium payments, and the policy will remain in force for the rest of the insured’s life.

With a 7-pay premium, the policyholder benefits from accelerated cash value growth within the first seven years of the policy, as the premiums paid during this time are typically higher than the cost of insurance. This means that a larger portion of the premium payments goes towards building cash value, rather than paying for the cost of insurance.

Advantages of a 7-pay premium IUL policy

There are several advantages to choosing a 7-pay premium IUL policy. One of the main benefits is the accelerated cash value growth that occurs within the first seven years of the policy. This can provide the policyholder with a significant cash value accumulation, which can be used for a variety of purposes, such as supplementing retirement income, funding a child’s education, or covering unexpected expenses.

Additionally, by opting for a 7-pay premium, the policyholder can secure a paid-up policy for life, without having to worry about future premium payments. This can provide peace of mind knowing that the policy will remain in force, regardless of any changes in the insured’s health or financial situation.

Furthermore, the cash value growth in a 7-pay premium IUL policy is linked to the performance of a stock market index, such as the S&P 500. This means that the policyholder has the potential to earn higher returns compared to traditional universal life insurance policies, which offer fixed interest rates.

Considerations before choosing a 7-pay premium IUL policy

While a 7-pay premium IUL policy has many advantages, it is important for potential policyholders to carefully consider their financial goals and needs before choosing this premium payment option. The higher premiums required in the first seven years of the policy may not be feasible for everyone, so it is important to ensure that the premium payments align with your budget and financial goals.

Additionally, it is important to understand that the cash value growth in a 7-pay premium IUL policy is subject to caps and participation rates, which may limit the potential for high returns. Policyholders should carefully review the policy terms and conditions, as well as consult with a financial advisor, to ensure that an IUL policy is the right choice for their individual financial situation.

In conclusion, an Indexed Universal Life Insurance 7 Pay Premium policy can be a valuable financial tool for those looking to secure a paid-up policy with accelerated cash value growth and the potential for higher returns. However, it is important for policyholders to carefully consider their financial goals and needs before choosing this premium payment option, and to consult with a financial advisor to ensure that an IUL policy is the right choice for them.