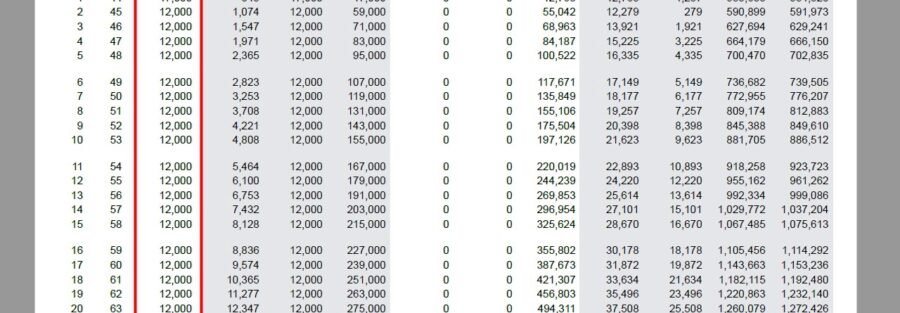

When it comes to comparing whole life vs Indexed Universal Life many people get it wrong! The products are designed to do …

[wpcode id=”4722″]

When it comes to choosing the right life insurance policy, individuals are often faced with a variety of options. Two popular choices are Whole Life Insurance and Indexed Universal Life (IUL) insurance. Both policies offer financial protection for loved ones in the event of a tragedy, but they have some key differences that need to be considered when making a decision.

Whole Life Insurance is a traditional form of life insurance that provides coverage for the insured’s entire life. It offers a guaranteed death benefit, as well as a cash value component that grows over time. The premiums are typically fixed and do not change over the life of the policy. This can provide a sense of security and stability for policyholders, as they know exactly how much they will pay each month.

On the other hand, Indexed Universal Life insurance is a newer, more flexible form of life insurance that combines the benefits of a permanent life insurance policy with the opportunity for cash value growth based on the performance of a specified stock index, such as the S&P 500. This means that policyholders have the potential to earn higher returns on their policy, but they also have some exposure to market risk. Premiums can vary and are often adjustable, giving policyholders more control over their policy.

So which is better, Whole Life Insurance or Indexed Universal Life insurance? The answer to this question ultimately depends on the individual’s unique financial goals and needs. Here are some factors to consider when making a decision:

1. Cost: Whole Life Insurance typically has higher premiums than Indexed Universal Life insurance. This is because Whole Life policies guarantee a fixed death benefit and cash value growth, while Indexed Universal Life policies have the potential for higher returns based on market performance. If cost is a major factor for you, IUL may be the better option.

2. Cash Value Growth: Whole Life Insurance policies have a guaranteed cash value growth rate, which can provide a stable and reliable source of savings over time. Indexed Universal Life policies, on the other hand, have the potential for higher cash value growth based on market performance. If you are looking for the opportunity for higher returns, IUL may be the better choice.

3. Flexibility: Indexed Universal Life insurance policies offer more flexibility in terms of premium payments and death benefit options. Policyholders can adjust their premiums and death benefits to suit their changing needs. Whole Life Insurance policies, on the other hand, have fixed premiums and death benefits that cannot be changed. If flexibility is important to you, IUL may be the better option.

In conclusion, both Whole Life Insurance and Indexed Universal Life insurance have their own unique advantages and disadvantages. It is important to carefully consider your financial goals and needs before choosing a policy. Ultimately, the best choice will depend on your individual circumstances and what you hope to achieve with your life insurance policy. Consulting with a financial advisor can help you make an informed decision that will provide the financial protection you need for your loved ones.